An interesting graphic from Bank of

Italy’s FinancialStability Review just released. The

graphic details collateral pledged to the Bank of Italy (“the Bank”) against

loans it has credited to counterparties in Eurosystem credit operations.

In part (a) “amounts” of the graphic we see levels of

overcollateralization at the Bank of Italy among its various counterparties in March 2012 and

August 2011. The blue is the amount

actually credit by the Bank to counterparties, the yellow is the value of

credit available to counterparties based on existed collateral posted (level of

overcollateralization) and the red is the Bank’s estimates of the net value of

unencumbered assets that are owned by counterparties and not pledged as

collateral to the Bank or elsewhere. All

of the amounts (in billions of euros) represent values net of haircuts, in

other words they do not represent the market value of the collateral but rather the value of credit available in Eurosystem repo operations based on the outstanding collateral.

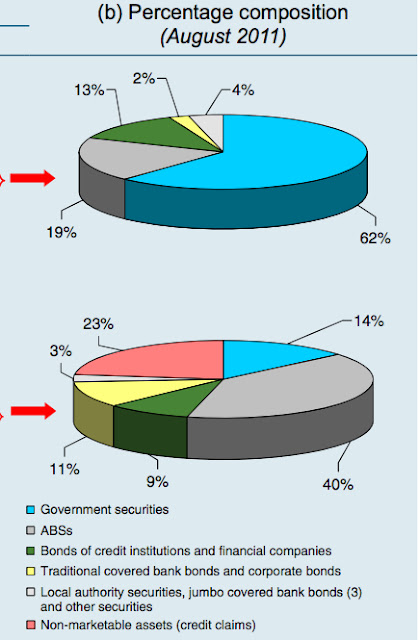

Part (b) details the composition of the collateral posted

with the Bank. The bottom pie represents

the share of the collateral actually posted with the Bank and the top pie

represents the share of unpledged collateral.

Some observations:

- The total amount of collateral posted to the Bank and freely

available grew dramatically from August to March, from 207 to 474 billion. Some reasons for this include an increase in

the available collateral due to ECB policy changes (extension of credit claim

collateral and lower ABS ratings permitted), and Italian government guarantees

for certain new bank issues. Other

possibilities include an increase in the total amount of securities available

(e.g. net issuance by Italian sovereign/banks) and a decrease in repo with

private counterparties freeing up more collateral.

- The amount of overcollateralization decreased from 48% in

August to 33% in March. Yet the fact

that Italian counterparties are still overcollateralized by 91 billion euros

with an additional 111 billion estimated by the Bank to be available based on outstanding collateral suggests the overall liquidity position of the Italian banking system

is not in acute crisis.

- Of

note, the large majority of the extra collateral resides with Italy’s biggest

banks (“5 main counterparties”) who collectively hold 67% of excess while only

representing 40% of borrowing.

- It

appears that the Bank has been successful in getting liquidity to smaller banks

as the amount of credit extended to “other Italian counterparties” increased

dramatically, from 28 billion in August to 123 billion in March.

- In terms of the composition of collateral,

the difference between collateral posted with the Bank and collateral freely

available is quite stark. While the vast

majority of eligible assets freely available (88%) are government securities,

the makeup of the pool of assets is a mixed bag.